Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowBy Cedric A. D’Hue, D’Hue Law, LLC

Indiana Code § 6-3-2-21.7 aims to encourage innovation by giving Indiana entrepreneurs and small businesses a break on Indiana state income tax. Several articles and blog posts initially notified the public about this unique Indiana tax benefit. A recent posting argued that all indications suggest this law is underutilized, essentially saying that Indiana patent owners are leaving money on the table. While I agree with some of the initial indications, I am encouraged by increased use of the law.

In my devotion to this law, I researched Indiana-based patents which may qualify for the Indiana patent income tax exemption. My search criteria involved identifying U.S. utility patents issued in the year 2008 to at least one Indiana individual or Indiana based business. My search criteria sought to exclude patents owned by large Indiana businesses or non-Indiana based businesses.

From this labor of love, my informal research identified two hundred and thirty seven (237) relevant Indiana based patents. It is reasonable to hypothesize that the law is underutilized when there are 237 potentially relevant patents and only ten Indiana taxpayers taking advantage of the law.

There are several reasons why so many patents might qualify for the exemption but only ten Indiana taxpayers took advantage of the law. First, it is unknown how many Indiana patent owners are aware of the tax law advantage. Second, I don’t know if each of the ten Indiana taxpayers utilized one or more patents when claiming their exemption.

Several factors might cause Indiana patent owners to not take advantage of this tax law. Not all U.S. patents immediately generate income. Another reason could be the cost associated with compliance of this law. For example, determination of fair market value of the licensing fees or other income generated from the sale of a product covered by the patent could easily exceed the tax savings provided by the first years of patent income. Intangible asset valuation firms may choose to charge $7,500 to $8,000 for an uncertified patent valuation and $20,000 to $25,000 for a certified patent valuation. A third reason is there can be a several year lag between filing a patent application and issuance of a U.S. patent. After notification about this unique tax benefit, Indiana entrepreneurs or small business owners may have filed for patent protection but have yet to receive an issued U.S. utility patent.

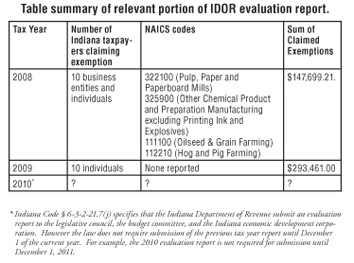

As illustrated in the Table, the sum of claimed exemptions almost doubled from 2008 to 2009 during one of the most challenging e conomic environments since The Great Depression. The increase has been encouraging. In my opinion the almost doubling indicates increased utilization in this unique Indiana tax benefit. I am interested to see if a pattern emerges and the increase continues upward for 2010.

conomic environments since The Great Depression. The increase has been encouraging. In my opinion the almost doubling indicates increased utilization in this unique Indiana tax benefit. I am interested to see if a pattern emerges and the increase continues upward for 2010.

In conclusion, the initial number of Indiana taxpayers utilizing this unique tax benefit seems to be small. Immediate and optimal use of this law would provide maximum benefit. Realistically, we may not see the full impact of this unique Indiana law for several years. Let us make the most of this opportunity by: (1) ensuring that all Indiana entrepreneurs and small business owners are aware of this exemption, (2) increasing our reporting on this law and continuing to evaluate its benefit to Indiana, and (3) assisting Indiana patent owners to take advantage of this unique tax benefit.•

Cedric D’Hue is a patent attorney and sole member of D’Hue Law LLC (www.dhuelaw.com). The opinions expressed in this article are those of the author.

Please enable JavaScript to view this content.